Climate change is a storm on the fast-approaching horizon. It’s already putting the health and safety of the crew at risk and is getting worse. Its high waves and strong winds threaten to make our journey turbulent and difficult.

To a large extent, the severity of the storm depends on the collective actions—or inaction—of the global community. The choice before the world—making rapid and deep cuts in emissions or letting global emissions continue to climb—will have a profound impact on the risks and opportunities that lie ahead.

At the same time, our own choices as Canadians matter. The ultimate success of our journey depends on our own actions and how we chart our course. Canada’s level of preparedness will influence how well we cope and manage with changing conditions. Canadians will be better off taking actions that anticipate change, limit risk, and lay the foundation to seize future opportunities. Our choices today and in the years ahead will have lasting impacts on current and future generations.

This section explores two climate scenarios for Canada. We use these scenarios to illustrate the broad range of challenges—and opportunities—that Canada could face with climate change and how understanding these challenges can better inform how we respond.

2.1 A SPECTRUM OF CLIMATE FUTURES

Canada’s climate future will be defined by two main external drivers. The first driver of change is the climate impacts resulting from increases in global GHG emissions. The more GHG emissions the world emits, the more frequent and severe physical impacts of climate change, such as heatwaves, wildfires, and sea- level rise, become. The second driver, which pulls in the opposite direction, is the extent to which countries decarbonize. The faster the world reduces GHG emissions, the faster market demand shifts away from emission-intensive goods and services.

The future will ultimately involve both types of change. The question, however, is which driver of change will dominate.

Possible climate futures lie along a spectrum of varying degrees of change. On the one end of the spectrum, rapid and deep cuts to global emissions (i.e., Deep Decarbonization) translate into moderate increases in global temperatures and, as a result, moderate climate impacts. However, ambitious and widespread actions to decarbonize trigger a transformational shift toward a low-carbon economy, bringing both new opportunities and risks. The world still faces the threat of more extreme climate events, but they are more manageable and predictable.

The other end of the spectrum, by contrast, paints a very different picture (i.e., Runaway Climate Change).

As global emissions increase, and as average global temperatures rise, the physical impacts from climate change become the dominant source of global change and disruption. The world experiences dramatic and potentially irreversible climate impacts, which, as we continue to emit GHGs, become worse and less predictable. The magnitude of social, economic, and environmental disruption is far greater as a result. The global economy still reduces emissions but the pace and scale is much slower and smaller.

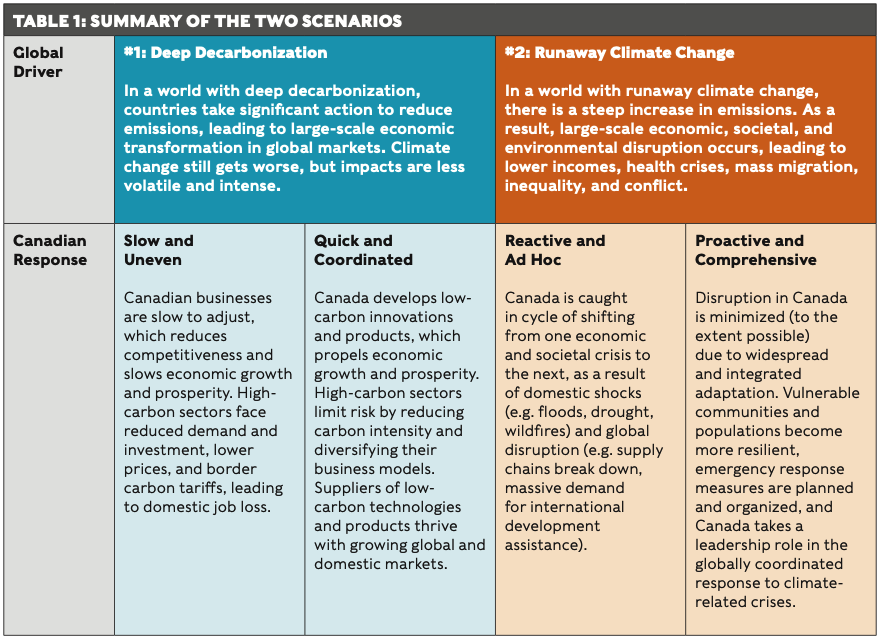

The analysis in this section focuses on the two extreme ends of this spectrum: Deep Decarbonization and Runaway Climate Change. We start by describing each scenario and the global trends that facilitate its trajectory. We then explore the different risks and opportunities each scenario could hold for Canada and how our choices can influence outcomes. For the Deep Decarbonization scenario, we focus on market risks and opportunities from global economic transformation. For the Runaway Climate Change scenario, we focus on the physical, economic, and societal risks of a changing climate. In each scenario, we describe two hypothetical cases: one where Canada is proactive and prepared, the other where Canada is reactive and ill-prepared (Table 1).

To inform our analysis, the scenarios in this section draw on a broad range of scientific and economic research. (1) They are, however, illustrations rather than predictions. We do not assess the likelihood of either outcome, or the range of outcomes in between the two scenarios. The scenarios are also necessarily simplified. Even with robust scientific evidence, it is uncertain how climate change will affect our economy, environment, and society. Other global trends (e.g., changes in population, environmental degradation, increasing living standards, technological advancements) interact with climate change and make such analysis immensely complex. Nevertheless, the scenarios shine a light on the key economic and societal pressure points from climate change, and how the choices made by Canadian governments, businesses, and individuals will affect our future.

2.2 SCENARIO #1: DEEP DECARBONIZATION

In the first scenario, the global community decarbonizes rapidly and achieves the emissions goal set out in the Paris Agreement: to keep the rise in average global temperatures well below 2o Celsius (C) above pre-industrial levels. Some extreme climate events still become more frequent and severe; however, the impacts are far less severe and disruptive relative to higher emissions scenarios (IPCC, 2018). (2)

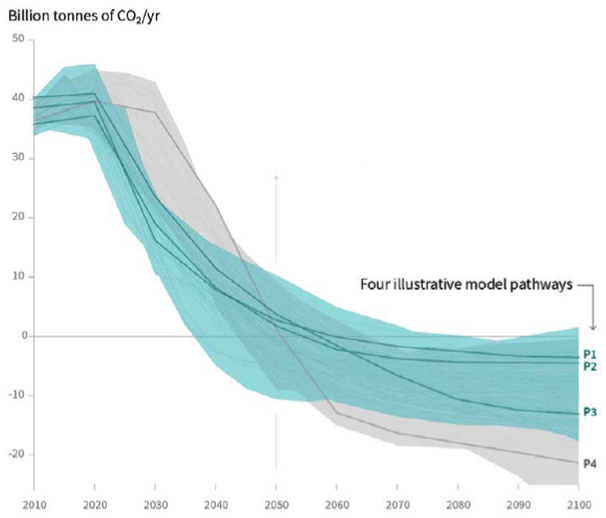

Limiting global temperature increases to well below 2o C requires rapid and significant cuts to global emissions and is much more challenging than achieving a 2o C goal. For example, while achieving 2o C would require global CO2 emission reductions of about 25% below 2010 levels by 2030, achieving 1.5o C requires reductions of around 45%. Figure 1 illustrates the different possible pathways to keep the rise in global temperatures to 1.5oC. Global emissions need to reach their peak between 2020 and 2030 and decrease rapidly after 2030. The world would also needs to achieve net-zero emissions between 2050 and 2060 and net-negative emissions thereafter (IPCC, 2018).(3)

The urgency and depth of emissions reductions required to achieve the Paris emissions goal trigger an economic transformation on a scale not seen since the first and second industrial revolutions. It represents deep emissions reductions across all sectors of the economy, including energy, heavy industry, agriculture, transportation, and manufacturing. The transformation unleashes unprecedented demand for low-carbon goods and services, triggering a significant shift in global markets.

FIGURE 1:

Global Emissions Pathways to 1.5° C

This figure shows several different emissions pathways to keep the rise in average global temperatures to 1.5o C above pre-industrial levels. Using historical emissions in 2010 as the starting point (measured in billion tonnes of CO2 per year), the analysis includes four different pathways (P1, P2, P3, and P4) out to the year 2100. Across all pathways, global emissions peak around 2020 and decrease rapidly thereafter. The world achieves net-zero emissions between 2050 and 2070 and net-negative emissions soon after. The lighter lines and shaded areas represent different ranges for each pathway.

Adapted from: IPCC, 2018

Although the exact timing and magnitude of these changes is uncertain, five main trends drive the transformation:

• Fossil fuel combustion is dramatically reduced. Keeping the rise in average global temperatures well below 2o C causes global demand for oil to peak by 2020, dropping by 27% below 2017 levels by 2040 (IEA, 2019a). The share of fossil fuels as a primary energy source drops from 80% in 2020 to less than 20% by 2100 (Shell, 2018). A large share of proven fossil fuel reserves become uneconomic as demand for fossil fuels sharply decline (McGlade & Ekins, 2015). (4)

• Electrification of key economic sectors such as manufacturing and transportation accelerates. The rate of replacing fossil fuels with cleaner sources of electricity triples by 2070 relative to 2018 levels (Shell, 2018; IEA, 2019a, 2019b, 2018a). More than half of global car sales are electric by 2030 and 100% are electric by 2050 (Shell, 2018). For light industry, the use of electricity doubles between 2020 and 2040, while the shift in heavy industry comes later, around 2050.

• An expansion of renewables largely displaces the sharp decline in the conventional use of fossil fuels. By 2040, 65% of global electricity generation comes from renewables (up from about 25% in 2016), driven mainly by growth in solar, wind, and bioenergy. Renewables become increasingly cheaper than fossil fuels by the 2020s and supply 40% of global electricity generation by 2040 (IEA, 2018a, 2019a). Nuclear power capacity triples between 2020 and 2070 (Shell, 2018).

• New low-carbon technologies emerge, disrupting markets and trade patterns. As the market for low-carbon goods and services grows, so too does growth in innovative low-carbon technologies. Breakthrough innovations are impossible to predict but can trigger positive feedback loops: a new low-carbon innovation can disrupt markets, which leads to yet more innovation and disruption (Lipsey et al., 2003). Cost- competitive fusion and hydrogen technologies, for example, could radically transform global energy systems. (5)

• Options to remove and capture carbon become more widely deployed. Achieving the Paris Agreement likely requires large-scale carbon removal from the atmosphere (IPCC, 2018, 2014). This means scaling up afforestation and reforestation, reforming agri-food systems, and greater use of direct air capture technology. Carbon capture, storage, and utilization will also be critical.6 By some estimates, this could require constructing some 10,000 large carbon capture and storage (CCS) facilities by 2070, compared to the 50 operating in 2020 (Shell, 2018).

Importantly, Canada still experiences the physical impacts of climate change in this low-carbon world; however, impacts are far less severe than in a future with runaway climate change (see next section). Historical emissions, and the additional emissions generated as the world transitions to a net-zero economy, will continue to increase global temperatures and cause the climate to change. While adapting and preparing for the physical impacts of climate change are critical to reducing disruption and damage from these impacts, the following two cases focus primarily on the risks and opportunities associated with a global transition to a low-carbon economy.

Canada’s Response: Slow and Uneven

In this version of the Deep Decarbonization scenario, Canada delays ambitious climate action and fails to prepare to compete in a low-carbon economy. Overall, high-emissions sectors do not reduce their emissions intensity or diversify, and companies developing low-carbon technologies and products struggle to commercialize and grow. Once global trends become apparent, it is too late to change investments in long-lived capital stock (e.g., buildings, vehicles, and equipment) or develop new low-carbon product lines that can compete against foreign firms that have been investing in research and development for decades.

The rapid transition globally, coupled with inadequate preparation domestically, creates large- scale disruption and job loss in Canada.

Much of Canada’s economy—and the prosperity it generates—depends on sectors that export emissions- intensive products and commodities such as oil and gas (Box 1). As global demand for fossil fuels drops, it leads to lower levels of investment in the sector. Oil sands projects are particularly affected, given their relative carbon intensity, timeframe to payout, and upfront capital cost (Leach, 2019). As a result, Canada’s oil and gas sector sees lower levels of revenue, profits, and employment. The hardest-hit firms are those that are slow to adjust to market trends and continue to depend on long-lived, emissions-intensive infrastructure and assets (Potvin et al., 2017; OECD, 2017).

BOX 1: RISKS TO CANADA’S OIL AND GAS SECTOR

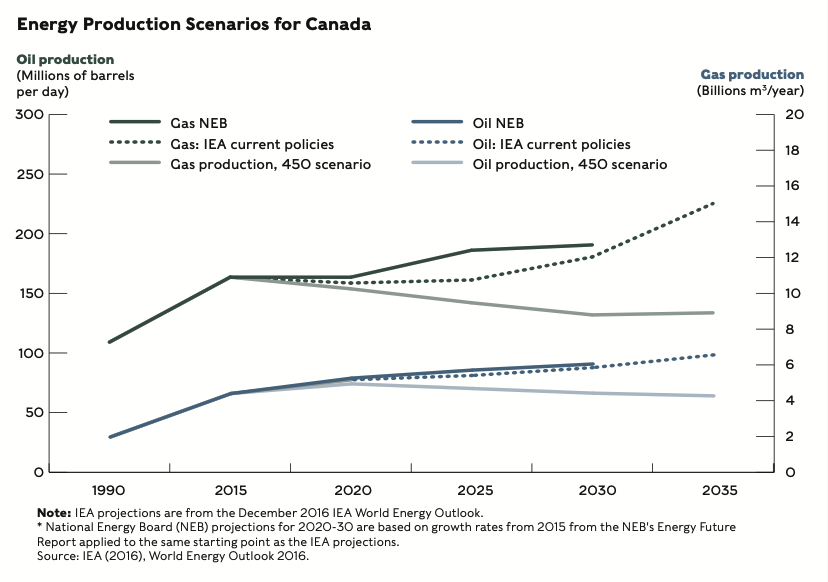

As global demand for fossil fuels declines, the market for Canada’s traditional energy exports shrinks. Energy scenarios produced by the International Energy Agency show Canada’s oil and gas production declining under a low-carbon scenario consistent with the 2° C goal (i.e., the 450 scenario in the figure below). In the longer term, well past 2035, the drop in global demand is likely to be more pronounced.

Canada’s oil and gas sector is highly exposed to such a dramatic change in global demand. In 2018, the sector accounted for 6% of Canada’s total GDP, provided roughly 1% of all jobs, and generated billions of dollars in government revenues. Yet emissions from this sector account for 25% of Canada’s total inventory. The oil sands represent 97% of Canada’s proven oil reserves, which are the third largest in the world. Crude oil from Canada’s oil sands is relatively carbon intensive and is among the most expensive types of oil to extract and refine. The financial sector is also exposed to risk from changes in this sector. The six largest banks in Canada held a combined $52 billion worth of outstanding loans to the oil and gas sector in 2019.

Sources: EPSF (2018, 2019); OECD (2017); World Bank (2019); ECCC (2018a); Statistics Canada (2019d); Natural Resources Canada (2018a, 2018b); Weber & Kholodova (2017); USGAO (2016); Bank of Canada (2019); Masnadi et al. (2018); Leach (2019).

Other Canadian sectors are also unprepared for the global shift in demand that puts a higher premium on low-carbon goods and services. They are slow to adjust to investor preferences and are caught off guard by export markets that erect trade barriers that penalize high-emissions imports. Emissions-intensive manufacturers in Canada, for example, become less competitive as other countries develop lower-carbon alternatives that are more attractive to markets facing increasing carbon constraints. Investors limit their exposure to carbon risk by favouring firms that are profitable in a decarbonized marketplace. Canada’s automotive industry, for example, sees plants close as a result of decreasing demand for gasoline-powered SUVs and light trucks, with vehicle manufacturing shifting to foreign plants that produce electric vehicles (Potvin et al., 2017; Yates & Holmes, 2019; Tanguay, 2018).

Over time, as global action mounts, the shocks to Canada’s most exposed sectors ripple throughout the economy. Lower incomes and weaker job growth in the oil and gas sector, for example, affect key sectors such as construction, manufacturing, retail, transportation, and real estate. Canada’s financial sector—heavily invested in fossil fuels—is exposed to greater risk as lending and investment in these assets weakens (Bank of Canada, 2019).

The rapid shift away from emissions-intensive goods and services also increases the risk of unemployment and widespread social disruption. Social support systems come under increased pressure (e.g., food banks, employment insurance, social assistance), particularly in communities that rely heavily on emissions-intensive industries (Mertkins-Kirkwood, 2018). Impacts are felt differently across provinces but occur from coast to coast, as many of the affected sectors employ Canadians from across the country (e.g., oil and gas workers in Alberta that live in Eastern Canada). Similar to coal communities in the Maritimes devastated by collapsing global demand in the mid- twentieth century, many small communities in oil-producing provinces (e.g., Alberta, Saskatchewan, and Newfoundland and Labrador) struggle with high unemployment and stretched government budgets that increasingly lead to cuts in health and education.

At the same time, Canada fails, in this scenario, to capture the opportunities associated with increased global demand for low-carbon technologies, goods, and services. With limited domestic demand, innovation from the private and public sectors is insufficient to develop leading technologies. In many respects, Canada becomes a technology-taker: it benefits from developments and innovations in other countries, but it loses out on the economic benefits associated with developing and exporting these technologies.

Inevitably, some progressive firms adapt and benefit from the shift in global demand, even without an early, coordinated and planned response. Increasing global demand sends clear market signals that lead to new investment strategies. Some mining companies, for example, increase copper and zinc production to respond to growing demand for metals and minerals needed for renewable electricity and battery production (Box 2). Relative to the next case, however, Canada fails to fully capture the opportunities available and leaves large segments of the economy at risk. Benefits are smaller and less widely distributed across the economy.

Canada’s Response: Quick and Coordinated

In this version of the Deep Decarbonization scenario, Canada is proactive and takes immediate and coordinated action to prepare for a low-carbon future. As a result, the economic transition for Canada is smoother and far less disruptive. Canada positions itself to capture growing market opportunities and to become a global leader in low-carbon innovation.

Importantly, early and coordinated action helps protect and improve Canada’s competitive edge in the global economy. High-carbon sectors make substantial adjustments to reduce emissions and diversify product streams, leaving them less vulnerable to sudden shifts in global markets. These actions also help insulate Canada from trade barriers that penalize carbon- intensive goods and services. Canadian firms are able to avoid border carbon tariffs and maintain—and even extend—their competitive advantage (Sawyer, 2013).

BOX 2: CANADA’S MINING AND FORESTRY SECTOR IN A LOW-CARBON WORLD

The global transition to a low-carbon economy could drive significant growth in some of Canada’s resource development sectors. Growing demand for solar panels, wind turbines, and battery storage, for example, could dramatically increase demand for key metals and minerals such as copper, iron, lead, nickel, zinc, cobalt, and lithium.

Canada is already one of the largest mining countries in the world, making it well positioned to benefit from this new global demand. Based on analysis by the World Bank, Canada has significant deposits of almost all metals critical for growth in clean technologies.

Canada’s forestry sector is also likely to benefit. In a low-emissions scenario, the use of bioenergy could double globally by 2050, putting forestry inputs in high demand. Biomass is also expected to become a much bigger input to consumer goods such as chemicals, plastics, food additives, and textiles. Canada is home to roughly 6% of the world’s bioenergy potential and is the second largest exporter of forestry products in the world.

Sources: CCFM (2017); FPAC (2017); OECD et al. (2017); Canada Senate (2018); World Bank (2017).

A rapid expansion of low-carbon energy is a key driver in Canada’s transition to a low-carbon economy. The supply of non-emitting electricity triples by 2050, driven by new investments in hydro, nuclear, wind, and solar power (Langlois-Bertrand et al., 2018).(7) At the same time, provincial agreements lead to new investments in inter-provincial transmission infrastructure that help share the benefits of low- carbon electricity projects. Provinces and territories historically dependent on fossil fuels (e.g., Alberta, Saskatchewan, Nova Scotia, New Brunswick, the Northwest Territories, and Nunavut) gain access to non-emitting electricity, driving significant emissions reductions.

The growth in non-emitting electricity generation helps electrify key sectors in the Canadian economy, such as buildings, agriculture, transportation, natural gas, and industry, giving Canadian products and services a low-carbon advantage in international markets. Several developing technologies also become more cost-competitive, such as second-generation biofuels and hydrogen fuel, enabling additional GHG reductions. Some segments of the economy eliminate the use of fossil fuels entirely, such as residential and commercial buildings and agriculture (Langlois- Bertrand et al., 2018; Weber & Kholodova, 2017).

Gains in energy efficiency and conservation play a supporting role, especially for households. Clean technologies, such as smart thermostats, heat pumps, and more efficient furnaces become cheaper and more widely deployed. These measures help keep total energy demand relatively stable over time, despite a growing population and higher incomes (Langlois-Bertrand et al., 2018; TEFP, 2016). Investing in efficient technologies and appliances also helps households reduce their energy bills.

Over time, the Canadian economy becomes more diversified and less susceptible to falling oil and gas prices. In the financial sector, investors diversify their portfolios quickly and on a broad scale, with a greater emphasis on low-carbon assets. Canada’s natural resource sectors also diversify their operations, with increased near-term focus on natural gas exports and longer-term investments in renewable electricity, hydrogen, and biofuels (Shell, 2019). Sectors such as oil and gas still suffer losses due to declining demand, but actions taken by government and business help these sectors diversify earlier, which makes the transition less disruptive.

At the same time, education and retraining programs help unemployed workers find employment in new and emerging sectors (OECD, 2015a). These programs reduce the risk of prolonged unemployment and social disruption, particularly in rural and small communities with local economies that are less diversified.

As the demand for emissions-intensive goods and services fades, the cleantech sector becomes a significant source of growth, innovation, and employment. Driven by surging domestic and global markets, Canada becomes a global leader in low- carbon innovation and a major exporter of low-carbon technologies, goods, and services. Meanwhile, resource sectors, such as mining and forestry, benefit from an unprecedented increase in global demand for raw materials used for clean technologies (Box 2).

2.3 SCENARIO #2: RUNAWAY CLIMATE CHANGE

Our second scenario considers a very different global context, where the international community does not take action to reduce emissions. Many countries do not meet existing emission reduction commitments and global GHG emissions rise rapidly. Global demand for energy continues to increase and is met by expanded coal, gas, and oil production. Renewable energy supplies some of this new energy demand, but fossil fuels play a dominant role.

Under this very high-emissions scenario, average global temperatures increase by as much as 5° C by 2100 (above pre-industrial levels).(8) Belatedly, after experiencing the devastating consequences of inaction, some countries start to make deep cuts in emissions. These efforts are too late to avoid severe impacts.

Economic and societal disruption increases significantly in this scenario. As extreme climate events around the world become more common, local economies suffer repeated shocks that dramatically reduce global income (by 6% to 10% annually according to some estimates). Vulnerable regions, such as Africa, suffer the biggest losses, where average national incomes fall by as much as 25%. These economic impacts cascade throughout entire economies, disrupting market demand, trade patterns, and supply chains. Parts of the world also experience severe food and water shortages, driving an increase in conflict, humanitarian crises, and mass migration in the most affected regions (Nordhaus & Moffat, 2017; Kompas et al., 2018, Dasgupta et al., 2007).

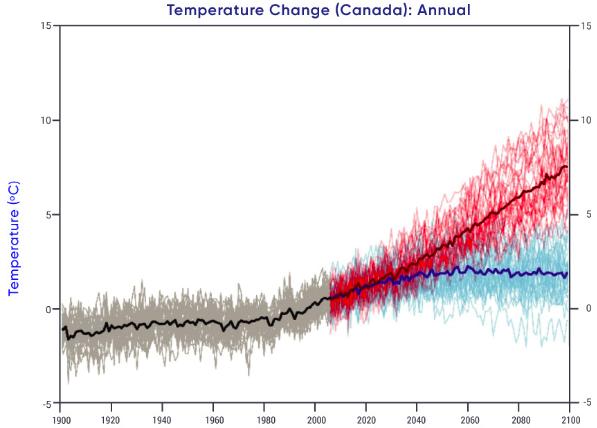

The continued rise in global emissions cause profound changes to local and regional climates in Canada. The dark red line in Figure 2 shows the implications for Canada in a very high-emissions scenario (ECCC, 2019a). By 2100, average annual temperatures rise an additional 5–10° C relative to pre-industrial levels, with even greater changes in the North.

The rapid increase in average temperatures causes significant disruption over the next century—far more disruption than we are currently experiencing from climate change and far more than in the first scenario. Extreme precipitation events intensify (in some cases by as much as 20%), particularly during winter months. With more rain and snow over shorter periods, combined with other non-climate factors, such continued drainage of wetlands and increasing rates of urbanization and paved (impervious) surfaces, flood risk increases significantly in many regions (ECCC, 2019a; Statistics Canada, 2016; Feltmate & Fluder, 2018; AAFC, 2015).

FIGURE 2: Annual Temperature Change (Canada, 1990 to 2100)

The grey lines in this figure show the (estimated) variations in temperature over the historical period (1900–2005); the solid black line represents the average over the same period. The dark red line represents average temperatures under a high-emissions scenario, based on the IPCC representative concentration pathway (RCP) 8.5. The dark blue line represents average temperatures for a low-emission scenario (RCP2.6).

Source: ECCC, 2019a

At the same time, many parts of Southern Canada become drier during summer months (ECCC, 2019a). Heatwaves become longer and more intense, causing an increase in severe droughts, water stress, and wildfires (Kharin et al., 2018; ECCC, 2019a). The chance of record-setting heat increases ten-fold by mid-century. By century’s end, Canadian glaciers lose more than 95% of their volume, based on 2006 levels (ECCC, 2019a).

Sea levels continue to rise, but at a much faster rate relative to the low emission scenario. By 2100, average sea levels in Atlantic Canada are as much as 100 centimetres higher and between 25 and 50 centimetres higher on Canada’s west coast.(9) These higher water levels increase the risk of extreme storm surges and flooding in Canadian coastal communities.

Ocean acidification increases at a faster rate, with devastating effects on some marine ecosystems (IPCC, 2014; ECCC, 2019a; NOAA, 2013).

Critically, there is a chance that impacts from runaway climate change are far worse than what this scenario describes. Climate impacts are non-

linear, where gradual changes (e.g., increasing ocean acidification) can cause sudden and unexpected changes (e.g., the rapid collapse of marine ecosystems or mass extinctions). In worst-case scenarios, positive feedback loops could push delicate and complex natural ecosystems beyond tipping points, causing irreversible and catastrophic damages (NRTEE, 2011; Yumashev et al., 2019; Schneider et al., 2019; IPCC, 2014).

BOX 3: THE HEALTH RISKS FROM HEATWAVES

The increasing risk of more extreme heatwaves illustrates the wide range of potential impacts to Canadians. Climate models suggest that as average temperatures in Canada increase, the chance of extreme heat increases dramatically. Even in moderate warming scenarios, the frequency of heatwaves in parts of Canada could more than triple.

The immediate impacts from extreme heat in Canada—like other climate impacts—will be felt most acutely by children, the elderly, and other vulnerable populations. More intense heatwaves are projected to increase mortality rates and will also increase the risk of other illnesses, like heat exhaustion and heat stroke. It is also expected to exacerbate pre-existing health conditions, such as asthma and cardiovascular disease. Over time, more frequent and intense heatwaves can trigger and exacerbate mental health issues, such as post- traumatic stress, anxiety, and depression.

Warmer temperatures are also projected to increase the spread of insect-borne illnesses and diseases, such as Zika virus and Lyme disease, as well as pests that affect agriculture and forestry.

Sources: Kharin et al. (2018); Carbon Brief (2018); Hayes et al. (2018); Decent & Feltmate (2018); Ryan et al. (2019); Government of Canada (2017); ECCC (2019a); Ebi et al. (2018); Bouchard et al. (2019); Bickis, (2019).

Canada’s Response: Reactive and Inconsistent

In this version of the Runaway Climate Change scenario, Canadians fail to adequately prepare for the severe impacts from climate change. The response is entirely reactive, and Canada becomes caught in a continual cycle of impact and recovery. Canada is hit from all sides, facing both localized physical impacts such as floods and drought, and economic impacts from global disruption.

A lack of preparedness increases health and safety risks to Canadians. In some cases, Canadians suffer direct physical harm from severe climate events that become far more frequent and intense, such as floods, wildfires, drought, storm surges, and heatwaves (Box 3). In other cases, impacts are indirect. Canadians experience poorer air quality from wildfire smoke, contaminated water from flooding, and other environmental factors. The economic effects of domestic and global disruption are also indirect, as affected investments lose value, companies lay off workers, and goods—food included—become more expensive.

The most vulnerable in Canada bear a dispropor- tionate share of these costs (Ebi et al., 2018; Health Canada, 2007). Those with more wealth and resources are better able to adapt and protect their families and property. Inequality in Canada increases as a result.

A lack of preparation also imposes massive, systemic risks to the Canadian economy. Being unprepared for longer and more intense dry periods, for example, lowers agricultural yields. Warmer air and water temperatures, coupled with ocean acidification, undermine the sustainability of Canadian fisheries. Hotter temperatures also increase the risk of forest fires and invasive species, such as the mountain pine beetle, threatening the sustainability of Canada’s forestry sector (ECCC, 2019a, Bickis, 2019).

Damages to public infrastructure and private property increase dramatically. Governments own and operate a large portfolio of infrastructure that is critical to the economy, including bridges, ports, roads, railways, water and wastewater facilities, communications infrastructure, defence and military installations, and transmission lines.

BOX 4: SEVERE FLOODS IN THAILAND ILLUSTRATE SUPPLY CHAIN RISKS

The increasing frequency and severity of extreme climate events, among other factors, is already disrupting global trade. The World Economic Forum, for example, estimates that weather-related disruptions to the production and delivery of goods and services are up 29% since 2012. Hurricanes and wildfires in North America were a key factor in this increase.

The severe flooding in Thailand in 2011 illustrates how a single event can disrupt global trade. In addition to the immense human and social cost inflicted by these floods, the economic cost was also significant. Flooding caused nearly 10,000 factories to close, reducing output by 36%. Some automotive assembly plants in Canada were forced to cut production by 50% due to a shortage in parts from Thailand factories. The floods also caused a worldwide shortage of hard drives, as Thailand produced 45% of the world market, causing global prices to double.

Sources: CBC News (2011); NOAA (2016).

Over time, extreme weather events compromise the effectiveness, lifespan, cost, maintenance, rehabilitation, and renewal of this infrastructure (Infrastructure Canada, 2018).

At the same time, extreme events impose larger damages on Canadian homeowners and businesses. Insurance premiums increase over time, making insurance unaffordable for the most vulnerable. As the costs from natural disasters mount, the entire private insurance industry comes under pressure. Government funding for uninsured losses and disaster relief continues to increase, meaning higher taxes and less spending on other public goods and services. Municipalities in particular come under increasing fiscal pressure (Giuzio et al., 2019; Dolynny, 2019; Feltmate et al., 2017; Armstrong, 2019).

Risks also extend beyond Canadian borders. Over time, more frequent and intense climate events make food and water shortages more common in other parts of the world, driving an increase in conflict, humanitarian crises, and mass migration. Although Canada is not directly affected by these events, it is overwhelmed with requests for assistance. For example, Canada is ill-equipped to deal with the sharp increase in migrants seeking refuge from the most affected regions of the world (IPCC, 2019).

Increasing levels of global disruption also create economic risks, which Canada is not prepared to manage. Many Canadian companies hold assets abroad and rely on complex, integrated supply chains to produce and deliver their goods (Wei & Chase, 2018). In addition to the immediate damages to property and disrupted operations, initial shocks cascade throughout entire supply chains. The price of imported foods, for example, increases substantially and some consumer goods and materials become unavailable (Box 4) (NOAA, 2016). Such shocks impose additional risks to Canada’s banks, which tighten lending and investment practices due to sudden and repeated spikes in climate-related losses (Bank of Canada, 2019).

Without protective measures, damage and degradation to Canada’s natural ecosystems becomes more widespread. Earlier spring melts and drier summers with hotter temperatures increase pressure on freshwater supplies, compounded by excessive water use. As a result, reactive measures become more common across Canada, such as emergency water restrictions. Extreme temperatures and weather events also damage other critical ecosystems, like wetlands and salt marshes, which provide both climate change and biodiversity benefits. Impacts to Canada’s North are particularly devastating, including the accelerated loss of loss of access to wildlife as a local food source and comprised infrastructure from permafrost thaw (IPCC, 2018; NCCC, 2019).

BOX 5: POTENTIAL OPPORTUNITIES IN A WORLD WITH RUNAWAY CLIMATE CHANGE

Some parts of Canada can capitalize on a high-emission scenario in the short term. Canada’s emissions-intensive sectors (e.g. oil, gas and chemicals) benefit from buoyed global demand, high commodity prices, and a delayed transition to a low-carbon economy. Rising incomes across developing countries could, for example, trigger an increase in demand for carbon-intensive sources of energy and raw materials, keeping commodity prices high and driving further investment in fossil fuels. These emissions-intensive sectors continue to benefit until the global community makes a belated attempt to decarbonize and broader economic losses affect energy demand.

As inhabitants of a cold and northern country, people living in parts of Canada could benefit from warmer temperatures. Warmer winters could, for example, result in fewer cold-related deaths and illnesses and lower heating costs for households and businesses. Warmer temperatures in spring, summer, and fall could also open new tourism opportunities that previously did not exist. Some farmers could benefit from warmer temperatures and longer growing seasons. And if agricultural production in other countries is hampered by extreme climate change, Canada could play a key role in meeting shortages in global demand.

Critically, any benefits in a high-emissions scenario are likely temporary and short-lived. Benefits diminish as extreme climate events become more common and intense. Fewer deaths due to extreme cold are offset by more deaths from extreme heat. Savings in heating bills are offset by increased use of air-conditioners in the summer. Longer seasons for growing crops are offset by an increase in heatwaves, droughts, and flooding. Potential benefits do not negate the need to prepare for risks.

Sources: Mintz-Woo & Leroux (2019); Carbon Brief (2018).

In many cases, governments are forced to replace these ecosystem services with costlier engineered alternatives. Examples include rebuilding Northern infrastructure to cope with sinking land, transporting clean water from further away, and physically moving species such as salmon to cooler waters. In extreme cases, ecosystems experience irreversible damage and collapse.

Canada’s rich biodiversity also suffers major losses in this scenario. The geographical range of species changes and shrinks, altering migration and breeding patterns and shifting the distribution and growth rates of species. On a larger scale, such drastic changes in climate alter entire food webs. And while plants and animals continuously adapt to changes in climate,

the rate and magnitude of disruption is much greater than in past millennia, increasing the risk of extinction (IPCC, 2014; 2019; UNEP, 2018; Bernier et al., 2019).

Despite widespread disruption from runaway climate change, some parts of Canada benefit in the short term (Box 5). These benefits, however,

are not evenly distributed or fully captured. Some Canadians face very high costs with no benefits, while others experience lower costs and greater benefits. Over time, benefits from a hotter climate become overshadowed by increasing disruption and instability. Canada also becomes more affected by extreme climate events in other countries, which increase trade disruption, create new health emergencies, and trigger mass migrations.

BOX 6: INNOVATIVE CLIMATE ADAPTATION

Countries around the world are innovating to adapt to climate change. The Netherlands, for example, is on the leading edge of flood risk and water-supply management. Over a quarter of the Netherlands is below sea level, exposing over half the country to flood risk. To address these risks, the country has adopted a comprehensive adaptation strategy, combining protection against flooding, drinking water security, and managing extreme heat or rainfall in cities.

Perhaps more impressive is that the Dutch integrate design, art, and livability into how adaption projects are built. These innovations have made the Netherlands world-renowned experts in flood-risk adaptation. The Global Centre of Excellence on Climate Adaptation is located in the Netherlands. Annual exports of water technology and expertise from the Netherlands have also doubled since 2000, adding over $10 billion to national GDP.

Sources: Ligtvoet et al (2015); NEAA (2019); Corder (2017); Delta Programme 2019 (2019).

Canada’s Response: Proactive and Comprehensive

In this version of the Runaway Climate Change scenario, Canada prepares itself for a future with extreme climate change. While there are still significant costs and risks to human health, Canadians do what they can to adapt to worsening climate change. Where possible, individuals, businesses, and communities make changes and investments that improve their resilience to the direct and indirect impacts of climate change. Canada also demonstrates leadership in managing global risks, such as destabilization of the financial system and large-scale humanitarian crises in Africa and India.

Actions that improve climate adaptation and resilience become widespread and integrated throughout Canada. Collectively, these efforts reduce the overall risk to Canadians, ensuring that businesses, households, and communities are less vulnerable to extreme climate events. Major health and safety risks described in the previous case are actively managed, as are risks to private property and public infrastructure (ECCC, 2019a).

Due to the wide range of climate risks across Canada—along with the unique context in each

community—various actions are taken to improve resiliency. Wildfire risk-reduction measures, for example, are implemented across high-risk areas, such as British Columbia and Alberta, to reduce the damage associated with fires. Better emergency response planning in these communities also helps reduce the likelihood of injury and death when wildfires do occur. Improvements in air filtration in buildings help protect communities, including the most vulnerable, from wildfire smoke. Wildfire prevention measures also become integrated with land- and water-use planning and asset management.(10)

Communities also become more resilient to flood risk. Resources focus on high-risk areas, involving large infrastructure projects such as engineered dykes, flood barriers, and stormwater infrastructure upgrades. More resources are also devoted to protecting and restoring natural ecosystems that provide flood protection and absorb carbon, such as wetlands, marshes, and forests. Canada takes its cue from other countries that are already adopting innovative adaptation measures (Box 6).

The number of people living and building in high-risk areas decreases and improved warning systems give residents more time to prepare when catastrophic events occur, reducing the risk of miscommunication and disorder. In extreme cases, some communities— particularly on the east, west, and northern coasts— are relocated to avoid costly damages from higher sea levels and more intense storm surges.

With additional support and incentives from governments, businesses take more direct actions to better understand and prepare for operational

and supply-chain risks. Farmers, for example, invest in smart irrigation systems to conserve water and manage fluctuations in precipitation. Auto manufacturers diversify their suppliers to ensure they are not overly reliant on vulnerable trade routes. At the same time, companies move to capture global market opportunities in countries seeking to manage climate change impacts. Water shortages, for example, drive an explosion of demand for water efficiency, desalination, and wastewater recycling technologies.

Adaptation measures also become more integrated into other government services. Social programs that protect the most vulnerable, for example, integrate the risk of extreme climate events directly into daily operations. This includes ensuring the homeless, seniors, pregnant women, persons with disabilities, and citizens who do not speak English are protected during intense summer heatwaves and get immediate assistance during severe storms or flooding.

2.4 SUMMARY

The scenarios illustrate that both global decarbonization and the physical impacts of climate change stand to profoundly affect Canadians. These changes—and our response to them—will affect almost every facet of our lives, from health care, drinking water, social services, public finances, and infrastructure to the types and availability of jobs.

Yet the two scenarios are bookends. In reality, aspects of both scenarios will matter for Canada. Some warming is inevitable, and so too are shifts in global markets in response to carbon constraints. Canada faces a future with elements of each.

Uncertainty is central to the challenges facing Canada. We do not know exactly how bad climate change will become, how fast the world will decarbonize, or even exactly how those impacts will play out in Canada.

As trends become clearer, governments and companies can adjust. However, many preparatory actions require long lead times that make waiting for certainty impractical. We cannot replace infrastructure, develop new technology, or diversify economies overnight.

As a result, Canada must make decisions today that lay a foundation for both futures. Canadians can thrive and prosper, but only if we make choices now that recognize the future risks and opportunities that we could face. Uncertainty is not justification for inaction; in fact, it is precisely the opposite. Being prepared requires action. Seizing opportunity requires making choices. Preparing for the future requires both preparing for a changing climate and preparing for a decarbonizing global economy. It requires comprehensive and integrated solutions that address multiple economic and societal risks outlined in both scenarios. Solutions, in other words, must help Canada be not only quick and coordinated as we build a strong, low-carbon economy, but also proactive and comprehensive in making that economy—and the people it supports—more resilient to climate impacts.

(1) The two scenarios notionally look out 50–80 years from today, but the exact timing and trajectory will vary under any scenario.

(2) This scenario assumes the international community achieves the goal set out in the Paris Agreement, keeping the average increase in global temperatures well below 2° C (above pre-industrial levels). Even with these deep cuts in global emissions, however, the world still experiences an increase in the frequency and severity of climate change impacts. Impacts already being felt—from increased heatwaves, flooding, wildfires, to sea-level rise—get worse, but are less severe than in our Runaway Climate Change scenario.

(3) There is a significant difference between the 1.5° C and 2° C temperature goals. Keeping the average rise in global temperatures to 1.5° C requires policy that is far more stringent, driving more rapid and wide-ranging disruption to the global economy. At the same time, the physical risks from climate change are substantially higher in a world with a 2° C increase in global temperatures (IPCC, 2018; Carbon Brief, 2018). The analysis in this section draws on various scenarios between 1.5° C and 2° C. Many of the scenarios consider pathways consistent with a 1.7 or 1.8 ° C temperature increase.

(4) Achieving a 2-degree goal could make a significant share of proven oil, gas, and coal reserves uneconomic, creating stranded assets. McGlade and Ekins (2015), for example, estimate that this means a third of global oil reserves, half of gas reserves, and over 80% of coal reserves cannot be used for combustion (assuming no technological advancements that significantly reduce emissions). Estimates by Citigroup suggest that the value of these stranded reserves is $100 trillion (Channell et al., 2015).

(5) Other technological advancements, new business models, and societal innovations will interact with climate-related technologies in different ways. The development of autonomous vehicles, artificial intelligence, block chain, and cloud-based services are a few examples of different emerging technologies that could have profound impacts on climate change.

(6) CCS technologies capture the carbon released during combustion (e.g., at an oil refinery) and deposit it underground, preventing it from entering the atmosphere. Carbon capture and utilization (CCU), by contrast, uses captured carbon to make new products, such as fuels, plastics, or cement.

(7) Technologies that are currently less commercially viable, such as second-generation biofuels and carbon capture and storage, could also play a role in this scenario.

(8) Temperature increase consistent with the representative concentration pathway RCP8.5, used by the International Panel on Climate Change, represents a very high-emissions baseline scenario (see our insert on the Scientific Foundations of Climate Change above) (Hausfather, 2019).

(9) The amount of sea-level rise experienced in coastal communities is, and will continue to be, different based on geography. This is due to the vertical movement of coastal lands. In some cases, like in Atlantic Canada, coastal land is gradually sinking (i.e., land subsistence), which amplifies the threat of sea-level rise. In other cases, like on Canada’s west coast, coastal lands are rising (i.e., land uplift), which helps offset the increase in sea-level rise (ECCC, 2019a).

(10) It should be noted that no amount of planning or resources can fully protect communities and individuals from the extreme climate impacts described in this scenario. While being prepared can reduce total costs, Canada would still experience widespread damage and disruption.